Are you aware that banks do not lend the full amount that you need for purchasing land, a house and lot or a condominium unit? Do you know what they are looking for when evaluating your loan application?

Let us discuss three important considerations used in determining how much you can borrow.

Loan-to-value ratio

The loan-to-value (LTV) ratio is critical as it determines the down payment or upfront amount that the borrower has to shell out when buying property. A higher ratio requires less cash-out while a lower ratio entails a higher out of pocket.

Banks use LTV ratio to reduce their lending risks. Sometimes referred to as “Margin of Financing,” the LTV ratio is expressed as a percentage and calculated by dividing the mortgage or loan amount by the collateral property’s appraised value. Simply stated, the amount that can be lent out is equivalent to the collateral property’s appraised value multiplied by the LTV ratio.

The setting of LTV ratios is affected by the borrower’s age, salary, personal and family income, savings, financial capacity and records of payment, as it relates to the bank’s policies. VIP clients and large developers’ buyers are preferentially given higher ratios because of their established relationships and good credit standing.

The type of property being purchased or used as collateral also determines the LTV ratio to be applied. Land is customarily assigned a lower ratio in comparison to house and lot, and condominium units.

LTV ratios range from 60 percent to 90 percent of the property’s appraisal value or total contract price of the real estate property. To illustrate, if the property is appraised at P6.25 million and allowed 80-percent LTV ratio, the buyer’s upfront amount is P1.25 million, while the loanable amount is P5 million.

Maximum loanable amount

On average, the maximum loanable amount is set at three times the borrower’s annual gross income.

If you are single, you can get a co-borrower, who will have joint obligation in paying the loan. A co-borrower need not be a relative although such a relationship will be assessed by the bank. Most importantly, your co-borrower should be able to show proof of income and good credit standing in order to support your loan application.

If you are married, you can add your spouse’s income to establish your family’s capacity to borrow.

Banks also allow you to indicate your supplementary income. However, you should disclose how much and where they come from, e.g. remittance from family members abroad, sideline incomes, interest from savings, etc.

To illustrate, you need to have a P1.67 million gross annual income to be lent P5 million, assuming a multiplier of three.

Amortization

Amortization refers to the combined principal (mortgage amount) and interest you need to pay each month over the loan term. Subject to their respective policies, banks will set your amortization roughly between 30 percent and 50 percent of your monthly gross income as banks believe that you should only spend a portion of your income on mortgage payment.

Amortization is influenced by the interest rate, whether fixed or variable. Under fixed-rate mortgage, the interest rate is consistent throughout the loan term. Variable-rate mortgage uses a fixed rate for a short period and thereafter re-adjusted annually. As of January 2022, private bank rates ranged from five percent to 12 percent for one to 20 years fixed, and varied with banks used, borrower’s credit worthiness, total loanable amount, banks’ relationship with their clientele and developers, and loan periods.

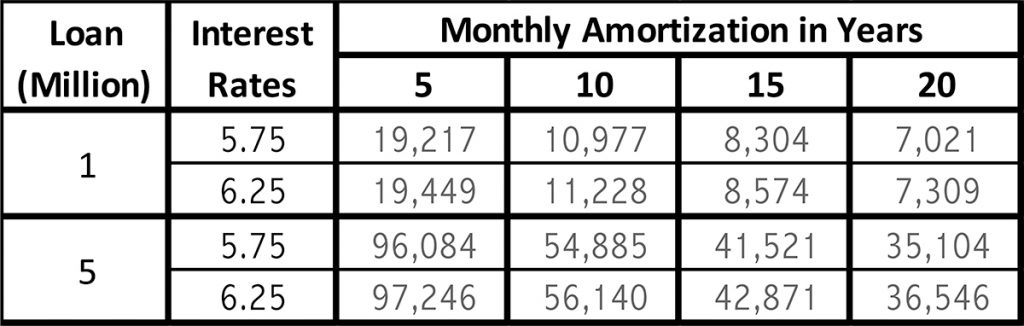

Below is a sample of monthly amortization based on four loan terms, two loanable amounts with two indicative interest rates each:

To illustrate, if you want to borrow P5 million at an interest rate of 6.25 percent fixed, and your bank is willing to set amortization at a third of your monthly gross income, you need P292,000 per month or P3.5 million per year to be eligible for a five-year loan, while your required gross income goes down to P168,000 per month or P2 million per annum if you opt for a 10-year loan.

Final amount

How much you can borrow is dependent on the above considerations, with the final loanable amount based on the lowest of the figures generated. Although there may be exemptions, knowing these respective limits allows you to understand the extent of your potential loan.

Most banks’ websites include a mortgage calculator to facilitate your self-assessment. Be prudent and shop for the best terms.

* * *

Henry L. Yap is an architect, environmental planner, real estate practitioner and former professorial lecturer.