Real estate is one of the industries which recorded surprising sales growth even after the pandemic struck last year. End-users realized the weight of having a safe shelter during a lockdown, while investors confirmed that crises could raise demand for property—being the end-all of investments—especially in the residential segment.

The government is attempting to bring this crisis-turned-opportunity trend to homebuyers across all market segments as the housing backlog continues to hover over the country, much like the current pandemic.

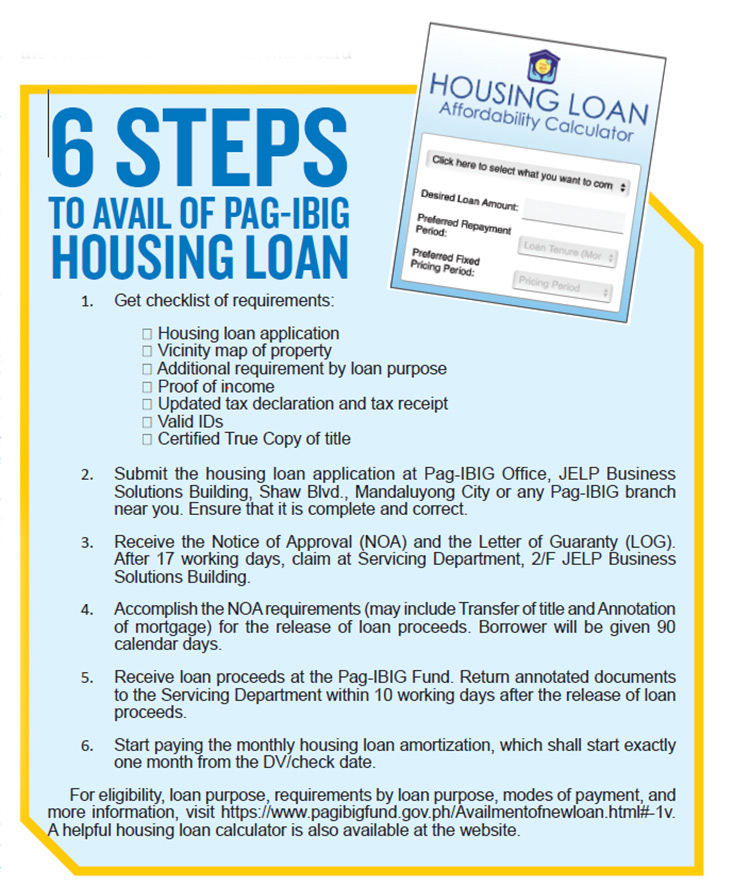

“For 2021, we are aiming to finance 19,854 socialized homes under the Affordable Housing Loan Program. We have set aside an amount of P8.6 billion for this so we can help our members who are minimum-wage earners or those who belong to the low-income sector buy or build homes for their families under a subsidized rate of only three percent per annum during the first five years of their loan term,” Pag-IBIG Fund CEO Acmad Rizaldy Moti tells Property Report PH.

The low rate applies to socialized housing loans up to P580,000 for house and lot packages and P750,000 for socialized condominium projects. This is available to members earning not more than P15,000 per month within the National Capital Region (NCR) and not more than P12,000 per month outside NCR.

Countryside housing

Pag-IBIG has also created Countryside Housing Initiative (CHI), where it partners with “local government units, employers, and other institutions to provide their chosen beneficiaries access to affordable but quality homes.”

“We have CHI projects all around the country, even in the remotest areas where no developer would dare to venture because of lack of demand. But because we have CHI, we have funded the construction of whole subdivisions in such areas to provide members with new houses which have sold for less than market value,” Moti adds.

After seeing a sharp decrease in housing loans in April and May 2020, the fund further reduced its already low interest rates—to just 5.375 percent per annum from 6.375 percent, for loans with a three-year repricing period and to just 4.985 percent per annum from 5.375 percent, for loans with a one-year repricing period.

At present, it is enhancing the Virtual Pag-IBIG to allow its accredited partner-developers to determine online if members seeking to purchase their housing units are qualified for a Pag-IBIG Housing Loan.

“I’d like to sum up by saying that Pag-IBIG Fund has significantly contributed to closing the gap of the housing backlog. In the 40 years of the Pag-IBIG Fund’s existence, we have released over P1.49 trillion in housing loans to finance homes of over 2.5 million Filipino workers and their families,” says Moti.

To match Pag-IBIG Fund’s low interest rates, the Department of Human Settlements and Urban Development (DHSUD) is streamlining processes and reducing operating costs for housing developers—to make housing more affordable.

“We are ensuring that the Ease of Doing Business Act is religiously observed and implemented by the Department, especially in the light of the recently issued RA 11517, which authorizes the President to expedite the processing of permits, licenses, and clearances in times of national emergencies,” says Secretary Eduardo Del Rosario in a correspondence with Property Report PH.

The department is also prioritizing the operationalization of the Housing One-stop Processing Centers (HOPCs), which can hasten the processing of permits and licenses at the regional level.

The DHSUD also fully supports Senate Bill No. 203, titled “An Act Providing for a National Housing Development, Production and Financing Program, Regularizing Its Appropriation for its Implementation.”

Once signed into law, the bill will appropriate P2.667 trillion to DHSUD and key shelter agencies for the implementation of the NHDPF Program over a 20-year period.

Key shelter agencies

The key shelter agencies and their tasks will be the following:

“National Housing Authority will be the lead agency tasked to develop and implement various types of housing programs intended for the bottom 30 percent of the income population, which includes resettlement, housing programs for low-salaried government employees, settlements upgrading, and housing programs of calamity victims, among others.

Social Housing Finance Corporation shall undertake social housing programs that will cater to the formal and informal sectors in the low-income bracket and to take charge of developing and administering social housing programs, particularly the Community Mortgage Program and its different modalities.

National Home Mortgage Finance Corporation is mandated to increase the availability of affordable housing loans to finance the Filipino home buyers on their acquisition of housing units through the development and operation of a secondary market for home mortgages.”

Partnering with the private sector

At present, the government is actively tapping the private sector developer groups to provide affordable housing to Filipinos.

“The private sector developer groups were likewise tapped to actively participate in the crafting of the National Housing and Urban Development Sector Plan which shall serve as the 20-year roadmap for the provision of adequate and affordable housing to all Filipinos. It will also serve as a guide toward a synchronized approach to urban development strategies across related stakeholders,” Del Rosario shares.

The department has given the developer groups access to participate in the National Human Settlements Board (NHSB), the single policy-making body for housing and urban development initiatives.

Low-interest rate environment

Speaking on behalf of the private sector, Organization of Socialized and Economic Housing Developers of the Philippines Inc. (OSHDP) chairman Marcelino Mendoza strongly urges the government to keep the interest rates low throughout the duration of the pandemic.

“The industry is thankful to Secretary del Rosario and President Moti for maintaining the concessionary low interest rate to housing borrowers. The government must also provide new windows to finance housing loan borrowers who have pending loan applications with private commercial banks, which undergo very slow processing,” he says.

He explains that the acceleration in the approval and release of housing loans would spur economic recovery as more funds would be plowed back into housing construction, creating new employment and setting off a multiplier effect to other industries.