Different sectors, different results. We have a mixed property prognosis for the next 12 months.

The office segment was able to breach our initial estimate as outsourcing firms and traditional occupants took up massive space the past 12 months. The Metro Manila condominium market surprised a lot of stakeholders, with net take-up rebounding significantly in Q3 2025 due to attractive promos offered by developers despite elevated bank mortgage rates. The retail sector has been the most resilient, backed by brisk take-up from foreign brands and mall developers’ aggressive refurbishment of retail spaces. International tourist arrivals YTD are subpar, with much of the recovery in hotel rates and occupancies due to strong local market. Meanwhile, we remain optimistic for the industrial sector with Philippine exporters projecting decent growth next year and as more foreign investment pledges materialize in 2026.

We expect 2026 to present a mix of headwinds and tailwinds, a normal occurrence for a cyclical Philippine property market. Developers need to future-proof their businesses to remain relevant in a constantly evolving real estate market.

Sustained office take-up

From 2026 to 2028, Colliers expects the delivery of nearly 350,000 sq meters (1.0 million sq feet) of new office space in Metro Manila, only a third of the 1.0 million sq meters (10.8 million sq feet) completed annually from 2017 to 2019, or pre-COVID and the peak of offshore gaming demand. We expect the Bay Area, Ortigas Fringe, and Quezon City to account for nearly 60% of the new supply.

Colliers expects average lease rates to remain stable in 2026. However, submarkets with below industry average vacancies, such as Makati CBD, Fort Bonifacio, and Ortigas Center, are likely to record marginal rise in rents.

We project Cebu to continue dominating transactions outside Metro Manila. However, with limited office supply in the pipeline (2026-2028, especially in CITP and CBP), there might be a slowdown in transactions. We also expect Pampanga to pick up momentum in the months ahead.

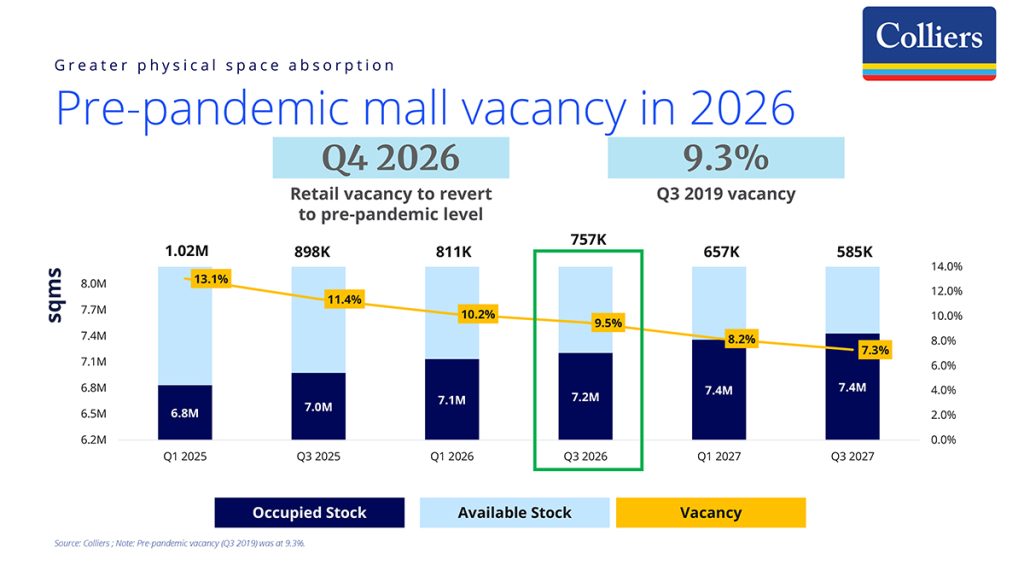

Impressive retail recovery to continue

In Q3 2025, Metro Manila retail vacancy further improved to 11.4% from 13.1% in Q1 2025. This is also the lowest since the 9.7% recorded in Q1 2020. Colliers retains its forecast that Metro Manila retail vacancy will revert to pre-pandemic level by the end of 2026. In Q3 2019, just before COVID, retail vacancy in the capital region reached 9.3%.

From 2026 to 2028, we expect the annual average completion of 111,000 sq meters of new retail space in Metro Manila, down from 332,000 sq meters delivered per year from 2017 to 2019.

The shift to suburbia has become more pronounced. Colliers data proves that property firms have been expanding their residential footprint outside of Metro Manila, and in our opinion, developers should complement these projects with the ideal size of retail component.

For instance, Rockwell will open Power Plant Malls in Angeles City and Bacolod City in 2027, while SM and Ayala Malls are setting their sights on key cities, including Cebu, Davao, Iloilo, and Bacolod, where new malls will be opened and renovated between 2026 and 2028.

Colliers expects food and beverage (F&B), clothing and footwear, and beauty and wellness retailers to dominate physical mall space take-up over the next 12 months. Foreign brands are also likely to continue occupying massive physical mall space.

Major developers have been earmarking billions for the reinvigoration of their retail centres, and this massive retail capex is also likely to benefit other growth areas outside Metro Manila, including Cebu and Pampanga.

To be continued.

#PropertyReportFeature

#FeaturedStory